As a card-carrying contrarian, I consider it my duty to counsel caution when people are getting over-excited – which I've been doing a lot of over the last few years, as property prices have steadily ticked upwards in most parts of the country, and rocketed in others.

This goes the other way too: when there's too much doom and gloom, I feel compelled to focus on the upside and remind people of opportunities they might miss if they're being too much of an Eeyore.

In 2018, I've got a feeling I'll be doing a fair bit of the latter. Starting right now.

(By the way, I'm not a literal card-carrying contrarian: why would I carry something just because someone else told me to?)

Short-term gloom

There's no doubt that property investment is less attractive than it was, because it's now tax-disadvantaged.

The new mortgage interest treatment means that property income is effectively taxed more punitively than any other type, and even capital gains from property are now taxed at a higher rate than other gains. Even if you buy property through a company to swerve the worst of it, you then get taxed when extracting the money from the company to actually do anything with it.

The media has picked up on this, and property as an investment is now getting dumped on from all quarters. This is compounded by projections for price growth being much slower than in previous years (many commentators are predicting only 1-2% growth in 2018, which would be a real-terms fall), rents stagnating, and signs that the low interest rate party is starting to come to an end.

This is all absolutely true. But it's also all temporary. And being deterred by these challenges means you risk missing the beneficial features of property investment that are permanent.

Long-term benefit #1: Index-linked rents

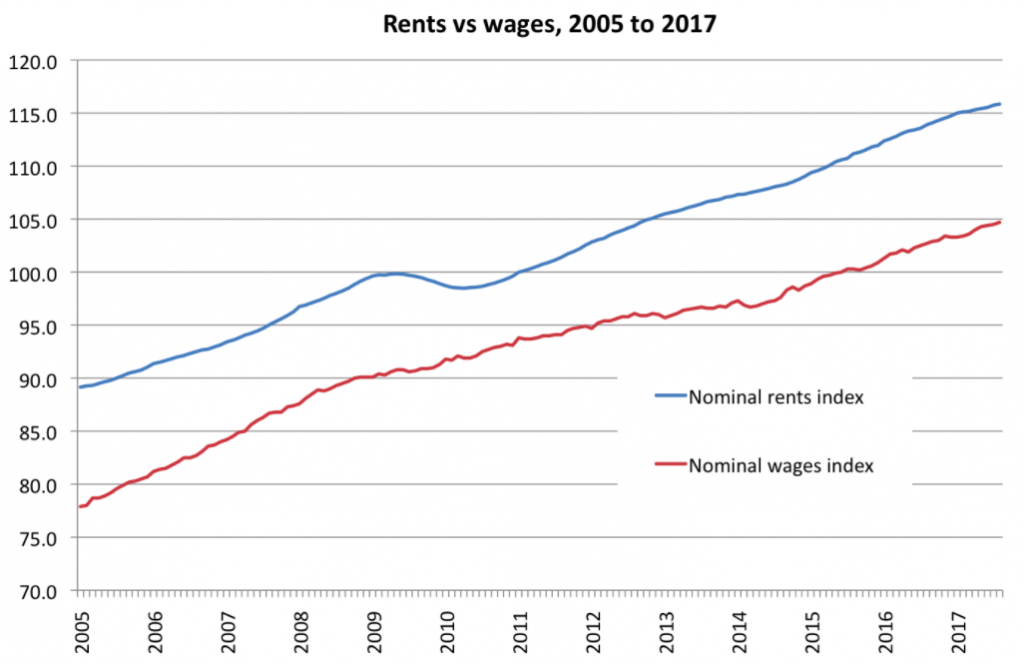

Rents are linked to wages, because it's somebody's wage that determines how much they can afford to pay for housing. Observe:

Although it hasn't been the case in recent years, wages generally rise in line with inflation. So when this link holds, it means that rents rise in line with inflation.

There are, obviously, about a zillion other variables that make this an imperfect correlation and mean that there are periods of time when it doesn't hold at all. But over the long term, it does.

What does that mean? If you've making £500 in rental income now, you can expect to be making the inflation-adjusted equivalent of £500 in 10, 20 or 30 years. In other words, the spending power of the rent you're receiving will be the same.

I don't know of any other asset class that can offer a consistent inflation-proof income over a span of multiple decades. That makes property a spectacularly good investment for retirement: you could retire at 60 funded by rental income, and still have the same spending power when you're 90.

Long-term benefit #2: Inflation-eroded mortgages

You borrow £75,000 to buy a house worth £100,000.

For the 25 year mortgage term, inflation runs at 2% per year.

The value of the house grows in line with inflation, so in 25 years is worth £164,000.

Your debt, meanwhile, is still only £75,000.

So leveraged property investment performs particularly well in an inflationary environment. So do other assets like gold and silver, but they don't pay an income – so again, property is unique.

And at the moment, you can borrow at sub-2% rates – meaning that the lender is guaranteed to make a real-terms loss, and implies that they're pricing in zero risk of default. Which is weird. But nonetheless, a great time to use leverage if you're doing so sensibly.

Keeping things in perspective

Yes, the government hates landlords.

Yes, property prices have run too far ahead and won't have much growth for the next couple of years.

Yes, stagnant wages mean that there's little scope for rents to rise.

But these factors are all temporary. The benefits, meanwhile, are permanent – as long as we spend more time in an inflationary rather than deflationary environment.

I'm not saying that property is the only asset class worth investing in – far from it.

I'm not saying that now is the time to throw caution to the wind and pile in.

I'm just saying that if you let the doom and gloom put you off holding any property in your portfolio, you'll miss out on the unique advantages that property has to offer.

So in a year when everyone's going to have an opinion about property and most of them are going to be negative, it's a particularly good time to focus on the long-term – and keep things in perspective.